Reviewing the Reporting Accuracy and Fiscal Effects of Industrial Revenue Bonds

Introduction

The Legislative Post Audit Committee requested this audit, which was authorized by the committee at its May 12, 2025 meeting.

Objectives, Scope, & Methodology

Our audit objective was to answer the following questions:

- What is the estimated fiscal impact of industrial revenue bonds to the state and local governments?

- What estimates are cities and counties that use industrial revenue bonds required to report to the Board of Tax Appeals on property tax exemptions and is that data accurate?

- How many foreign companies have received industrial revenue bonds?

To answer these questions, we interviewed officials and reviewed information from the Kansas Board of Tax Appeals (BOTA), the Kansas Departments of Revenue (KDOR), Labor, and Commerce, the Kansas Secretary of State, and several local governments across the state.

For Question 1, we analyzed data on industrial revenue bonds (IRBs) issued and IRB property tax exemptions (IRBXs) approved from 2010 through 2024 to determine the number of IRBs issued and IRBXs approved, the total value of the IRBs, and a high-level estimate of forgone property tax revenue at the state and local levels.

For Question 2, we reviewed the cost-benefit analyses (CBAs) for a judgmental selection of IRBXs to determine how closely the estimated amount of forgone tax revenue aligned with actual forgone property tax revenue. We reviewed 23 IRBXs from 5 local governments out of 399 IRBXs issued during 2013-2023 across 89 local governments. We chose these IRBXs and local governments to include a mix of large, medium, and small cities; a county board; and a unified county-city government, as well as a range of large and small projects. Because our selection was judgmental rather than representative, the results can’t be statistically projected to the population of IRBX applications or local governments. However, the results are likely indicative of issues extending beyond the 23 IRBXs we reviewed.

For Question 3, we used data from BOTA, the Secretary of State, and the Departments of Labor and Commerce to identify foreign companies that received proceeds from IRBs in 2024. More specific details about the scope of our work and the methods we used are included throughout the report as appropriate.

Important Disclosures

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Audit standards require us to report limitations on the reliability or validity of our evidence. In this audit, limitations in the reliability of the IRBX data provided by KDOR limited our ability to report some county-level information. We found some data inconsistencies in the county-level IRBX data that KDOR could not fully explain. However, the statewide totals appeared reliable and followed expected trends. Because of this, we report on statewide trends rather than exact county-level values. Additionally, KDOR has limited data on sales tax exemptions, which prevented us from estimating the fiscal impact of that portion of the IRB program.

Our audit reports and podcasts are available on our website www.kslpa.gov.

During 2010-2024, local governments issued about $18.3 billion in industrial revenue bonds and exempted about $1.1 billion in related property taxes, most of which likely would’ve gone to school districts and local governments in the state.

IRB Program Background

Local governments issue industrial revenue bonds (IRBs) to help finance business facilities to promote economic development in their communities.

- The Legislature created the IRB program to improve the state’s economy and overall well-being by attracting new businesses and helping existing businesses grow or remain in the state. The Kansas Legislature first authorized cities to issue IRBs in 1961 and later expanded this authority to counties in 1981. The Kansas Development Finance Authority can also issue IRBs, but this is rarely done.

- Local governments, including the boards of county commissioners and the governing body of any city, can issue IRBs to help fund business facilities in their communities. Their goals often include growing the local economy and increasing property tax revenue by helping businesses build, expand, equip, or remodel facilities. Some programs focus on certain industries, like aerospace or healthcare, while others support goals such as historic preservation, infrastructure improvements, or workforce development. Statute allows nearly any industry to use IRBs.

- Businesses use IRBs to finance their projects and are responsible for repaying them. Typically, local governments and businesses enter into a lease or lease-purchase agreement when IRBs are used. In this arrangement, the local government owns the property financed by the IRB as collateral and leases it back to the business while the bonds are being repaid. The business makes lease payments, which are used to pay off the bonds. State law (K.S.A. 12-1743) prohibits local governments from using tax revenues to repay IRBs. Bond agreements between local governments and businesses include terms that govern what happens if the business defaults on the agreement.

- Businesses using IRBs benefit from lower interest rates than other funding options like loans or other bond types. Businesses with IRBs can also qualify for other benefits such as property tax and sales tax exemptions.

IRB projects can qualify for a property tax exemption (IRBX) for up to 10 years.

- In Kansas, real property (e.g., land and buildings) and certain personal property (e.g., machinery and vehicles) are taxable. However, with limited exceptions, K.S.A. 79-201a allows property financed with IRBs to receive a property tax exemption for up to 10 years on the portion of the property financed with the bonds. This report refers to this exemption as an IRBX.

- Local governments determine whether to offer an IRBX and establish the terms of the exemption. Not all IRB-financed projects receive an IRBX, and exemption percentages, durations, and eligibility requirements vary by jurisdiction. For example, Lawrence generally offers a 10-year, 50% property tax exemption, while Wichita offers an initial 5-year exemption that may be extended for an additional 5 years and adjusts the exemption level based on factors like capital investment and job creation.

- Local governments administer IRBXs with limited oversight from the Board of Tax Appeals (BOTA) and reporting by the Kansas Department of Revenue (KDOR).Cities and counties have dedicated economic development staff, city managers or administrators, or contracted legal staff who work with businesses to understand the project scope and determine the exemption terms. The city council or county commission reviews and may make final adjustments to the terms. We refer to these officials and governing bodies as local governments. Although local governments may require additional steps, state law requires IRBXs to go through the following steps:

- Before issuing IRBs, K.S.A. 12-1744a requires local governments to file an informational statement with BOTA that describes the project and the bond terms. If a local government plans to offer an IRBX for the project, the local government must indicate that on the informational statement. BOTA records the data from the informational statement and assigns a reference number to it (called a docket number).

- Under K.S.A. 12-1749d, if a local government plans to offer an IRBX they must also prepare a cost-benefit analysis (CBA) and notify affected taxing entities such as school districts. The local government is required to complete these steps before it issues the IRBs.

- To get approval for an IRBX, the local government first applies to the county appraiser. They must submit an application that includes the BOTA docket number from the informational statement and CBA among other items. The county appraiser reviews the IRBX application and verifies the property’s value and eligibility. Then the county appraiser sends the IRBX application to BOTA along with their recommendation to approve or deny the IRBX.

- BOTA makes the final determination on whether to approve or deny the IRBX. BOTA reviews the county appraiser’s recommendation and the application to verify that the local government submitted all the required documentation, and the project satisfies statutory requirements. BOTA assigns a new docket number to the IRBX application and approves or denies the exemption. BOTA is not statutorily required to evaluate the content of the application to determine whether the project is a sound economic development investment.

- After BOTA approves the exemption, the local government must file yearly claim forms with the county appraiser to confirm that the property still qualifies for the IRBX. State law does not direct BOTA to monitor or oversee IRBXs after BOTA issues its tax exemption decision. KDOR is only required by state law to collect and report IRBX data.

- Personal property generally isn’t included in the IRBX application and approval process because it’s exempt by statute. State law (K.S.A. 79-223) has exempted most commercial and industrial personal property (e.g. machinery and equipment) from taxation since 2006. As such, the amount of personal property exempted through IRBXs has decreased significantly as the incentive has become unnecessary. In the IRBX data we reviewed, personal property accounted for a small percentage of the total property exempted under IRBX. Thus, the forgone property tax revenue estimates presented later in this report primarily reflect exemptions on real property.

IRB projects can also qualify for a sales tax exemption for IRB-financed project costs.

- Kansas levies a 6.5% state sales tax plus additional local sales taxes of up to 5% on many purchases of goods and services. Sellers collect the sales taxes from buyers at the time of purchase and remit them to KDOR. KDOR distributes the sales tax revenue to the appropriate taxing entities that levied the tax.

- State law (K.S.A. 79-3606) includes many exemptions from Kansas sales tax, but for this audit we reviewed only K.S.A. 79-3606(d) because it specifically relates to IRB projects. This statute allows purchases made with IRB funds, including personal property such as construction materials and certain services, to be exempt from state and local sales taxes. The exemption is typically valid for the duration of the IRB project. The exemption ends when the project ends.

- To make tax exempt purchases, the local government that issued the IRBs applies for and receives a project exemption certificate from KDOR. The local government can then provide the certificate to the project developer who gives it to their suppliers or service providers at the time of sale to be exempted from sales tax. A sales tax exemption doesn’t require a CBA nor review by the county appraiser or BOTA.

IRB Issuance Trends

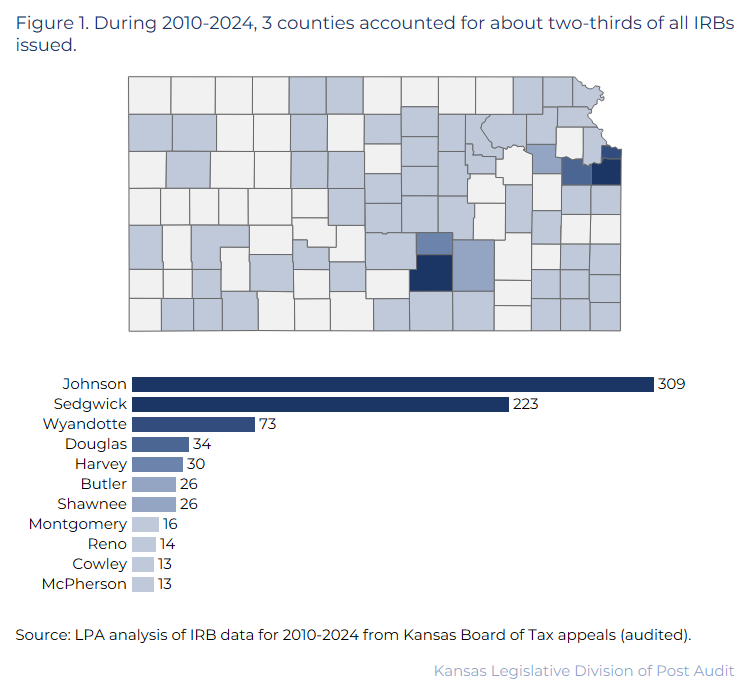

During 2010-2024, local governments issued about 955 IRBs worth about $18.3 billion, primarily in larger counties.

- We reviewed IRB data that BOTA derived from the informational statements local governments submit to determine how many IRBs were issued during 2010-2024. During this period, local governments issued about 955 IRBs with a total value of about $18.3 billion.

- Figure 1 shows where IRBs were issued during 2010-2024. As the figure shows, most IRBs were issued in and near Kansas City and Wichita. Overall, 60 of 105 Kansas counties (57%) had at least 1 IRB during 2010-2024 and 45 counties (43%) had no IRBs. About two-thirds of all IRBs were issued in Johnson, Sedgwick, and Wyandotte counties. The other 57 counties accounted for the remaining one-third of IRBs.

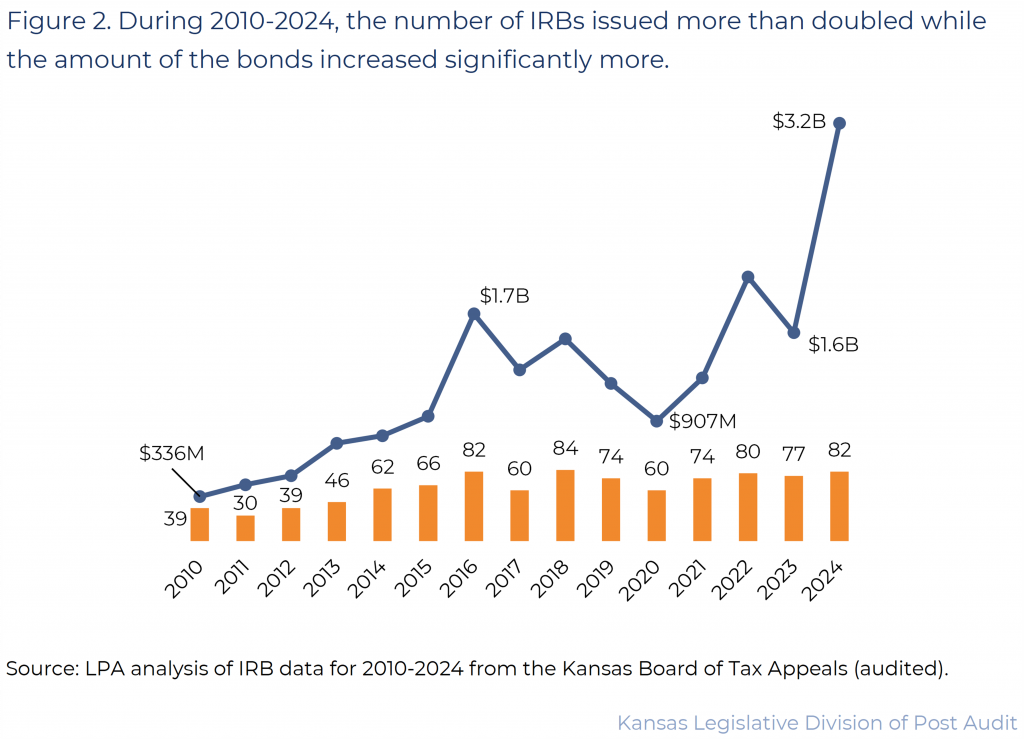

The number of IRBs issued increased at a modest pace during 2010-2024, but the total dollar amount of IRBs issued rose substantially more.

- Figure 2 shows the trend in IRB issuance and IRB amounts (e.g. the amounts that must be repaid when the bonds mature, not including interest) during 2010-2024. As the figure shows, the number of IRBs issued over that period more than doubled from 39 to 82. The largest IRB was issued in 2022 for $403 million for the construction of an Urban Outfitters distribution facility in Kansas City. The smallest IRB was issued in 2018 for $30,000 for Wesley Medical Center in Wichita to refinance an IRB previously issued in 2013. State law (K.S.A. 10-116a) allows IRBs to be issued to refinance other IRBs.

- Although the number of IRBs issued has been relatively consistent in recent years, Figure 2 shows the amount of IRBs has increased significantly. From 2010-2024 the total amount of IRBs issued per year increased from $336 million to $3.2 billion. Much of this growth occurred in 2024.

- A significant portion of the increase in the total amount of IRBs in 2024 was driven by 3 major projects that accounted for over $1 billion in IRBs. These included $300 million for a dairy processing facility in Dodge City, $350 million for a bottling and canning plant in Olathe, and $375 million for a soybean processing facility in Cherryvale.

IRBX Fiscal Impact: Property Tax Exemptions

Appraised values, assessment rates, and mill levies are used to determine the annual tax amounts for real property.

- The following formula determines the amount of real property tax that is levied on a property: Real Property Tax = Appraised Value of Property × Assessment Rate × Mill Levy ÷ 1,000.

- Appraised Value: Each Kansas county has a county appraiser who determines the value of all real property in the county each year. Appraisers use several methods to estimate property values. For example, they may look at sales of similar properties, the cost to replace buildings on the property, or rental income the property generates.

- Assessment Rate: An assessment rate is the percentage of a property’s appraised value that can be taxed. In Kansas, assessment rates range from 11.5% to 33% based on the type of property. Residential property is taxed at 11.5%, while commercial and industrial property is taxed at 25%. For example, if a commercial property is appraised at $100,000, its assessed value would be $25,000. Property taxes would be based on that amount.

- Mill Levy: State and local governments use mill levies to determine how much tax is levied on the assessed value of a property. State and local governments determine the mill levies unless the levy is specified in statute. For every $1,000 of assessed value, a taxpayer pays $1 for each mill levied by a taxing entity. For example, the average mill levy for real property in Kansas in 2024 was about 127. That means, on average, a taxpayer paid about $127 in real property taxes for every $1,000 of assessed value on their real property in 2024. In the previous example, it means the taxpayer would pay about $3,175 in taxes on the $25,000 of assessed value for their commercial property.

We estimated statewide forgone property tax revenue from IRBX using data provided by KDOR.

- We estimated the fiscal impact of IRBXs from 2010 through 2024 using data KDOR collects from counties on exempt property values. We found some data inconsistencies within certain counties that we couldn’t fully explain. However, the statewide totals appeared reliable because they followed expected trends. Therefore, we report on statewide trends in this audit rather than exact county-level values. We discuss the county-level inconsistencies we identified later in this report.

- To estimate forgone property tax revenue, we used statewide appraised values for the IRBX-exempted property in each county. We assumed that most IRBX-exempted properties would have been assessed at the 25% commercial and industrial assessment rate if they were not exempt. Then, we multiplied those assessed values by the average mill levy in each county because property-specific levies were unavailable. For example, we estimated the forgone IRBX property tax revenue in Johnson County using Johnson County’s average mill levy.

- These estimates should be viewed as approximate. Mill levies vary within a county based on the taxing jurisdictions applicable to a property, such as cities, school districts, library districts, and fire districts. As a result, properties within the same county may be subject to different effective mill levies. In addition, some projects may qualify for assessment rates that differ from the 25% commercial and industrial rate assumed in our analysis. These assumptions explain why the numbers in this report should be considered estimates.

- Finally, we estimated how forgone revenue would have been distributed among the state, counties, cities, school districts, and other local taxing entities. We also accounted for payments in lieu of taxes (PILOTs), which some businesses pay to partially offset forgone property tax revenue. We considered PILOT amounts to be reductions in the amount of forgone property taxes.

During 2010-2024, BOTA approved about 520 IRBXs which reduced statewide property tax revenues by an estimated $1.1 billion.

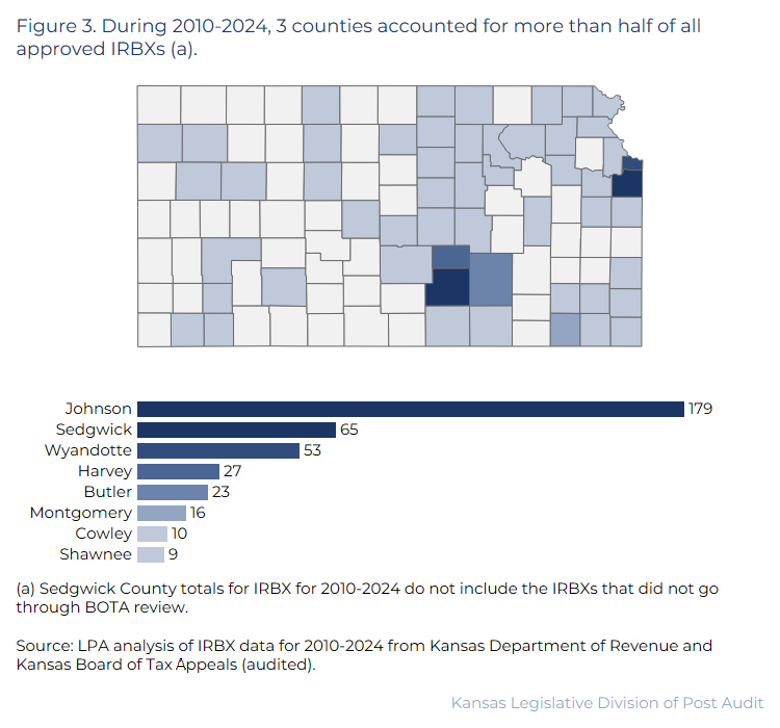

- During 2010-2024, BOTA approved about 520 IRBXs. Figure 3 shows where IRBXs were approved during that period. Like IRBs, the figure shows that most IRBXs were in and near Kansas City and Wichita. Overall, 53 of 105 (50%) Kansas counties had at least 1 approved IRBX during 2010-2024 and 52 counties had none. More than half (57%) of the IRBXs were in Johnson, Sedgwick, and Wyandotte counties. The remaining 50 counties accounted for the remaining 43% of approved IRBXs.

- The number of IRBXs in Sedgwick County is undercounted because the county appraiser’s office did not submit many IRBX applications to BOTA for approval during that time. We discuss this issue in more detail later in the report.

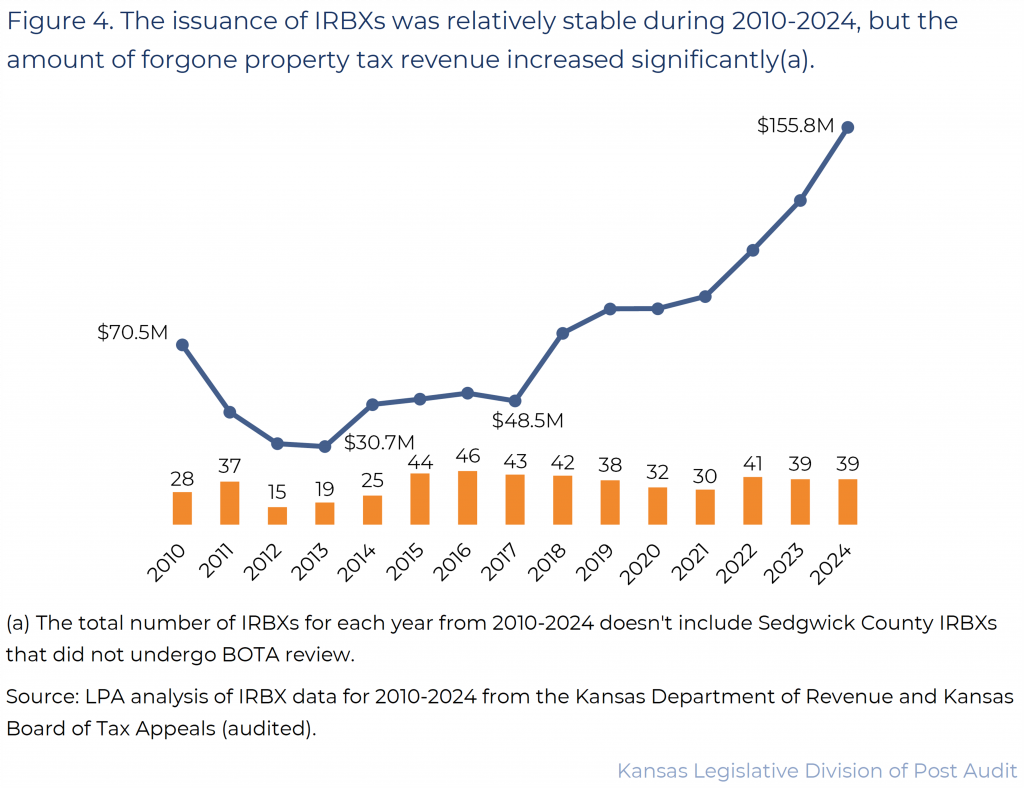

The number of IRBXs approved was relatively stable during 2010-2024, but the amount of property tax exempted increased significantly.

- After accounting for PILOT payments, we estimated IRBXs may have reduced property tax revenues across the state by up to $1.1 billion for the period 2010-2024. Johnson, Sedgwick, and Wyandotte counties accounted for two-thirds of the forgone taxes (about$724 million or 66%). The 50 other counties that had approved IRBXs during that period accounted for the remaining one-third (about$374 million or 34%).

- Figure 4 shows the trend in IRBXs approved and the estimated amount of forgone property tax revenue from IRBXs during 2010-2024. As the figure shows, the number of IRBXs approved was relatively stable. Following a dip in IRBX approvals in 2012, the number of IRBXs increased and was relatively stable between about 30 and 45 each year between 2015 and 2024.

- As the figure also shows, the estimated amount of forgone property tax revenue during 2010-2024 due to IRBXs increased significantly from about $31 million per year in 2012 and 2013 to about $156 million in 2024. The steepest increase started in 2017.

- We didn’t investigate why IRBXs increased. It could be due to a combination of factors, including increasing IRB project values and recent inflation in commercial property values in the counties where most IRBXs are including Johnson, Sedgwick, and Wyandotte counties.

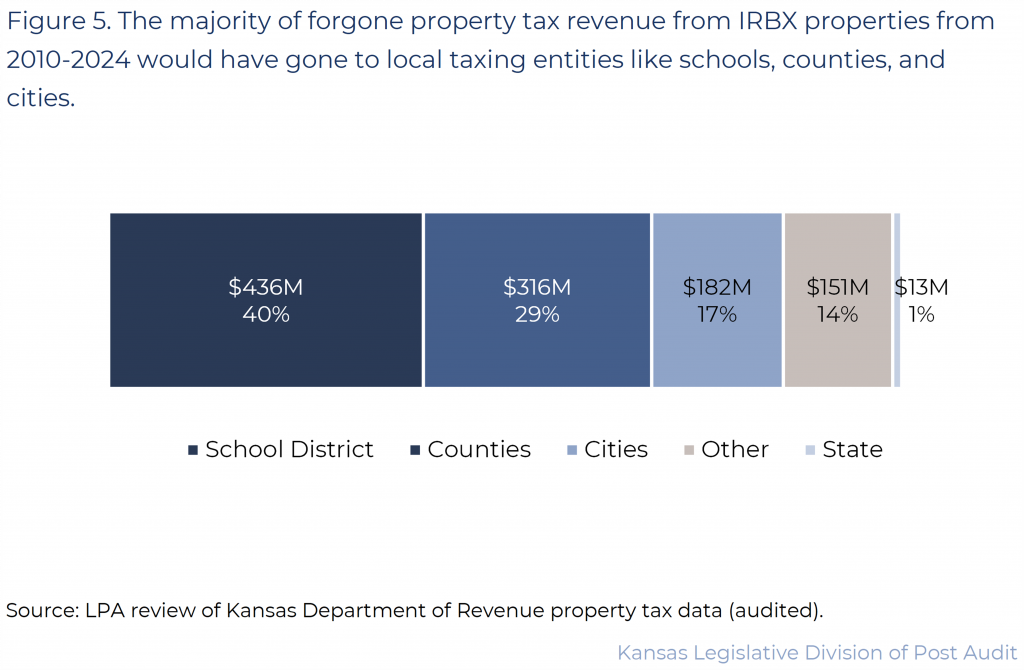

Most forgone property tax revenue from IRBX-exempt properties would have gone to school districts and local governments with the state receiving only about 1%.

- Most property tax revenue goes to local governments to fund local services. Only about 1% of all property taxes collected in Kansas go to the state. The rest go to local taxing entities, including counties, cities, townships, and school districts based on tax rates largely set at the local level. Local governments use this money to fund services like roads, parks, fire and police departments and public schools. Counties collect all the property taxes, send the money to the state and local taxing entities, and report each year to KDOR about how the money was distributed.

- We used property tax distribution data from KDOR to calculate the average distribution of property taxes across state and local government from 2010 – 2024. We then used those averages to estimate how much forgone IRBX property tax revenue would have gone to the state, counties, cities, school districts, and other local taxing units.

- Figure 5 shows how the estimated $1.1 billion in forgone property tax revenues for 2010-2024 would’ve been distributed. As the figure shows, the largest amount would’ve gone to school districts followed by counties, cities, and other local taxing units (e.g., townships, water and hospital districts, libraries, parks and recreation funds). Only $13 million (1%) would have gone to the state.

- The state and local taxing entities forgo tax revenue when properties are tax exempt. But this doesn’t mean the state and local taxing entities would’ve received $1.1 billion more in property taxes during 2010-2024 if the projects hadn’t received IRBXs. That’s because it’s likely that at least some portion of the projects would not have developed the way they did had they not received an exemption. Thus, these estimates should be viewed as the maximum potential forgone property tax revenue.

IRB Fiscal Impact: Sales Tax Exemptions

Data limitations prevented us from evaluating the forgone sales tax revenue for IRB projects during 2010-2024.

- KDOR publishes annual estimates of forgone state sales tax revenue. The forgone tax revenue is broken out by the statute that allows for the exemption. The law that exempts IRB properties (K.S.A. 79-3606(d)), also exempts hospitals and schools from sales tax.

- We spoke with KDOR officials to determine if we could use their data to estimate state and local sales tax exemptions specific to the IRB program but learned that was not possible. KDOR’s computer system is not designed to track sales tax exemptions by individual program or to estimate local sales tax exemptions because the agency is not required to do so by law.

- As a result, the forgone property tax estimate presented earlier in the report likely understates the IRB program’s total fiscal impact on the state and local governments from 2010-2024 by hundreds of millions of dollars.

- Collecting sales tax exemption data for specific programs would require changes to current reporting processes. This could be done by changing how sellers track and report exempt purchases to KDOR. Developers and local governments could also provide information on exempt project purchases to KDOR. Either approach would require significantly more tracking, reporting, and staff time from businesses, local governments, and KDOR, which may make such changes infeasible.

Other Findings

State law requires BOTA to approve IRBXs but allows properties to be exempt from taxation while IRBX applications are being processed.

- State law (K.S.A. 12-1744a)requires local governments to file an informational statement with BOTA that describes the project and the bond terms before issuing IRBs. BOTA requires the local government to indicate on the informational statement whether they intend to offer an IRBX. BOTA reviews the informational statements to ensure they’re complete and assigns a reference (docket) number to them.

- State law (K.S.A. 79-213) requires local governments that want to request an IRBX to first submit an application to their county appraiser. The application needs to include the docket number for the corresponding informational statement. The county appraiser reviews the IRBX application, verifies the property’s value and eligibility, recommends to approve or deny the IRBX, and forwards the application and recommendation to BOTA. Statute (K.S.A. 79-213) requires BOTA to make the final determination on whether to approve or deny the IRBX.

- State law (K.S.A. 79-213(i)) allows taxpayers to stop paying tax on the subject property while the county appraiser and BOTA are reviewing the IRBX application, beginning on the date the application is filed with the county appraiser. If the IRBX application is denied by BOTA, the taxpayer is required to pay taxes that accrued during the review period starting 30 days after BOTA’s decision. If BOTA approves the application, the property is officially declared exempt.

The Sedgwick County Appraiser’s office didn’t submit many IRBX applications to BOTA for approval over the past 30 years as required by state law.

- TheSedgwick County Appraiser’s Office reported to us that they recently discovered some IRBX-exempted properties had not been approved or denied by BOTA. They said that a former official accepted IRBX applications and classified the properties as exempt but then didn’t submit many of the applications to BOTA for approval. The former official sent some IRBX applications to BOTA but not others and current officials couldn’t explain why.

- County officials told us they’re still assessing the situation, but that as of May 2025, they had identified at least 112 IRBXs dating back to 2015 that didn’t have BOTA approval. However, they said this may have been an issue for up to 30 years. The county appraiser can’t determine how many of the IRBXs granted before 2015 didn’t receive BOTA approval because the 10-year exemption period is closed. We reviewed several of the IRBXs the county identified and confirmed they didn’t appear in BOTA’s IRBX data.

- County officials told us the local governments sent the required informational statements to BOTA for the IRBs associated with the 112 IRBXs they had identified. We didn’t confirm that BOTA received all 112 informational statements, but we did review several of the IRB docket numbers the county appraiser provided to us and confirmed they were in BOTA’s IRB data.

- Officials also said they had identified at least 18 exemptions issued through the Economic Development Exemption program (EDX) that weren’t approved by BOTA. Because EDX was outside the scope of this audit, we didn’t examine the issue further. Officials from the Sedgwick County Appraiser’s Office estimated that the backlog of 112 IRBX and 18 EDX applications could take them 2 to 3 years to process.

Poor segregation of duties at the Sedgwick County Appraiser’s Office, unclear timelines, and a lack of state agency oversight allowed this situation to happen.

- County officials explained to us that the former employee worked on IRBX applications for 30 years with no involvement from other county staff. The officials couldn’t explain why the employee didn’t send all IRBX applications to BOTA or why the practice was allowed to happen for so long. But they told us they implemented a team review process for IRBX applications after they discovered the issue.

- BOTA doesn’t have a monitoring process that would allow them to identify if they received all IRBX applications they should have.

- BOTA officials told us they rely on counties to follow filing requirements and that they don’t have the statutory authority or resources to investigate or penalize counties that don’t comply. As a result, BOTA didn’t identify Sedgwick County’s filing problems because they were not monitoring whether all anticipated IRBX applications were being submitted. In addition, the former county official was submitting some IRBX applications, which did not raise concerns that other required applications were possibly missing.

- The informational statements associated with unsubmitted IRBX applications included information that could have helped BOTA match them to later IRBX applications and identify cases where an expected application was never filed. However, statute (K.S.A. 12-1744a) only requires BOTA to collect these statements and make sure they are complete. It does not require BOTA to use them to track whether a related IRBX application is later submitted. If BOTA used informational statements to help them identify unfiled IRBX applications, their review would not catch all issues immediately. That’s because IRB projects may take several years to build or may be delayed or cancelled.

- Finally, state law and regulations create uncertainty regarding the timing of the application review process. State law doesn’t establish a deadline for county appraisers to forward IRBX applications to BOTA. Because property taxes are not collected while an IRBX application is pending, if a county appraiser delays forwarding an application, a taxpayer may not pay taxes on a property for multiple years before BOTA issues a final decision.

This issue could affect some Sedgwick County businesses’ property taxes and the quality of BOTA’s IRBX data.

- For active IRBXs in Sedgwick County that weren’t approved by BOTA, BOTA officials said they’d work with the county appraiser to retroactively review the applications. If BOTA denies an application, the business would resume paying property taxes on the subject property. It’s unclear if the business would resume paying taxes moving forward or if they also would be required to pay back taxes for previous years. Sedgwick County Appraiser officials told us they thought it could require paying back taxes. Regardless of BOTA’s decision, the businesses or Sedgwick County would likely have to pay BOTA a $500 to $1,000 filing fee that’s required by state law.

- This issue means that BOTA’s IRBX and EDX records are incomplete for Sedgwick County, but the effects could be much bigger or more widespread if similar issues exist in other counties and programs. We didn’t conduct an in-depth evaluation of the controls for approving and issuing property tax exemptions in Kansas. However, statute assigns BOTA the authority to approve or deny many types of property tax exemptions in the state, not just IRBX and EDX. It’s possible that appraisers in other Kansas counties also may not have submitted all IRBX or other property tax exemption applications to BOTA for approval. We did not determine if this issue existed in other counties because it was outside the scope of this audit.

We identified county data that was inconsistent or missing from KDOR’s reports.

- State law (K.S.A. 79-1477) requires KDOR to support the administration of tax laws by developing and updating a statewide property tax data system and publishing annual statistical reports. Because of this responsibility, KDOR’s reports should contain accurate information so users can properly understand property tax activity in Kansas.

- As part of our audit work, we identified several issues with KDOR’s tax data and reporting. We compared KDOR’s Statistical Report of Property Assessment and Taxation to its abstract system and county CAMA data. That work showed missing or inconsistent property values for tax-exempt properties and payment in lieu of tax (PILOT) amounts.

- The CAMA system (Computer-Assisted Mass Appraisal) is software that counties use to manage, analyze, and value property for taxation. County appraisers use it to appraise properties and store detailed parcel-level information such as ownership, building data, sales history, and valuation calculations. This system is controlled by the counties, but KDOR can query the system to provide us with data.

- The abstract system is KDOR’s statewide reporting framework used to summarize property tax data each year. Annually, counties summarize their CAMA data into several abstract reports which they submit electronically to KDOR. Rather than storing detailed parcel records, the abstract system organizes property values into general classes like residential, commercial, and industrial.

- KDOR uses abstract system data to create their annual Statistical Report of Property Assessment and Taxation (statistical report) which reports property tax data, including property tax exemptions, across the state.

- In our data reliability work, we found cases where exempted property values in the statistical report matched the abstract data but not the CAMA data. In other cases, we found the CAMA data matched the abstract data but not the statistical report, or that none of the data sources matched. Because all 3 sources are based on the same data, we would expect all 3 sources to match.

- The issues didn’t appear to reflect a statewide problem with KDOR data. But we did see repeated inconsistencies in certain counties. Some of the differences were large and spanned multiple years. For example, Cowley County’s abstract values of exempted property from 2020 through 2024 were between 64% and 3,600% higher than the statistical report values. Similarly, Finney County’s exempt values in the abstract system from 2018 through 2024 ranged from $36 million to $49 million, while the statistical report showed no IRBX exempt property values during those years.

- We also found that the statistical reports were missing PILOT values from 2020 through 2024 for Johnson and Wyandotte Counties. PILOT amounts for Johnson County were underreported by at least $41.7 million, and Wyandotte County’s PILOTs were underreported by $8.7 million. As a result, statewide PILOT totals over those years was understated by at least $50.5 million.

- We worked with KDOR to identify and correct data errors when possible. However, it is unlikely that we identified and corrected every error. Errors that may have a large impact within a single county may have little effect on statewide totals. For example, a $10 million error in 2024 could have a significant impact on the statistics for an individual county but would have accounted for less than 0.2% of the approximately $5.3 billion in statewide IRBX exempt property value that year. Because of this, we chose to present results only at the statewide level rather than the county level.

KDOR’s data issues were likely caused by county-level errors and insufficient review during the creation and submission of annual abstract reports.

- KDOR officials said the process of sending and processing the county abstract reports is a labor-intensive process that’s been vulnerable to human error. KDOR officials said that errors like the ones we identified were likely caused by counties incorrectly reporting information to them. KDOR officials said they perform basic data checks on the data that counties submit, such as verifying that control totals in their system match county reports. But they said they don’t have enough resources to review all county-submitted data at a detailed level. Staff focus on taxable property data because that’s the property that generates revenue. As a result, errors may go unnoticed.

- It’s important for KDOR to improve its data quality checks because anyone using KDOR’s statistical reports could misunderstand how much property was exempt under IRBX and how much of the exempted taxes were offset by PILOT payments.

Local governments are required to submit a cost-benefit analysis that estimates forgone property tax revenue when applying for an IRBX, but those estimates differed substantially from the actual forgone revenue for 23 projects we reviewed.

Background and Methodology

State law requires local governments to prepare cost-benefit analyses (CBAs) if they want to offer IRBXs but provides limited guidance on their content or quality.

- With limited exceptions, state law (K.S.A. 79-201a) permits property financed with industrial revenue bonds (IRBs) to receive a property tax exemption (called an IRBX) for up to 10 years on the portion of the real or personal property funded with IRB proceeds.

- State law (K.S.A. 12-1749d) requires local governments to prepare a cost-benefit analysis (CBA) if they plan to offer an IRBX for a project. State law does not require a CBA for projects that only receive IRBs.

- Statute requires local governments to complete the CBA before they issue the IRBs. CBAs are intended to estimate future economic and fiscal impacts of IRB-funded projects. State law only requires CBAs to include the effect of the IRBX on state revenues. It does not establish any criteria for how to define or determine that CBA results are accurate. For example, state law does not require local governments to compare CBA estimates with actual outcomes and determine whether the estimates were accurate.

- In practice, CBAs also often include more information than required. For example, they may estimate the project’s fiscal impact on other taxing jurisdictions, such as cities, counties, and school districts. CBAs may also include estimates for job creation and other economic benefits and costs. This audit focused only on estimates of forgone property tax revenue. We didn’t compare other projections to actual outcomes.

- In practice, local governments may prepare the CBAs themselves, or they may use the services of outside parties. This means that CBAs may vary significantly in terms of content and assumptions. In this audit we reviewed CBAs created by 4 different entities. One local government prepared CBAs themselves, but the other local governments used third-party consultants.

Our 2022 audit of the IRBX program found significant differences between CBA estimates of forgone property tax revenue and actual forgone revenue data from county appraisers in a sample of 8 CBAs.

- In 2022, LPA audited the IRBX program and estimated the economic and fiscal impacts of 8 IRBX projects over a 30-year period. Part of that work compared CBA estimates for forgone property tax revenue with actual amounts reported by county appraisers.

- That audit found that forgone property tax revenue estimates in 6 of the 8 CBAs were between 18% and 266% different than the county appraisers’ amounts. The 2 remaining IRBXs were still active at the time, but auditors estimated that they’d likely end up being significantly different too.

- Legislators requested this audit as a follow-up to the 2022 audit results. In this audit, we reviewed a larger number of CBAs to determine if the findings from the 2022 audit applied to a larger number of projects, including more recent IRBXs.

We selected 23 IRBXs from 5 local governments to determine how their CBA estimates of forgone property tax revenue compared to actual amounts.

- Using BOTA’s IRBX data, we identified 89 local governments that applied for 399 IRBXs from 2013–2023. We limited our review to IRBXs approved in these years to balance the availability of knowledgeable staff and the status of the IRBX. For example, older projects have more complete years, but staff are less likely to recall what assumptions they used in the CBA, whereas newer projects have fewer complete years, but staff are more likely to recall details about how the CBA was created.

- We reviewed a judgmental selection of 23 IRBXs issued by 5 local governments to identify differences between CBA estimates of forgone property tax revenue and actual forgone tax revenue amounts provided by county appraisers. The local governments included Lenexa, Olathe, Park City, the Shawnee County Board of Commissioners, and the Unified Government of Wyandotte County and Kansas City, Kansas. We initially included Wichita but removed them because their CBAs didn’t provide year-by-year estimates. The local governments we reviewed in this audit were different than the local governments we reviewed in the 2022 audit, except for the Unified Government of Wyandotte County and Kansas City, Kansas.

- We selected CBAs and local governments to represent a mix of government sizes and types as well as a range of large and small projects. The results can’t be statistically projected to the population of 399 IRBXs approved during 2013-2023 or to the 89 local governments that applied for them because the ones we selected aren’t representative of the population. However, the results are likely indicative of issues beyond the 23 IRBXs we reviewed and builds on the sample work in LPA’s 2022 IRBX audit.

- To determine actual forgone property tax revenue amounts, we worked with county appraisers to collect and verify appraised values, assessment rates, mill levies, and payments in lieu of tax (PILOT) payments for each project through 2025. For each project year, we calculated forgone property tax revenue using the standard property tax formula: Forgone Property Tax = Appraised Value of Exempt Property × Assessment Rate × Mill Levy ÷ 1,000. We used assessment rates provided by county appraisers. We then subtracted PILOT payments because they offset forgone property tax revenue.

- Of the 23 IRBXs we reviewed, 8 were complete and 15 were still active. For completed projects, we compared estimated and actual amounts of forgone property tax revenue for the full exemption period. For active projects, we evaluated only completed years through 2025. We didn’t project outcomes for the remainder of the exemption period. For example, if an active IRBX project had an exemption period of 2021-2030, we were only able to evaluate the first 5 years of the exemption.

- We interviewed local officials and CBA preparers to better understand how they develop their estimates and why estimates of forgone property tax revenue differed from actual amounts. For this audit, we used county appraiser values to calculate forgone property tax revenue. We did not review how county appraisers calculated their values or if they were reasonable. But the appraisal process involves judgment and some amount of uncertainty, which may help explain some differences between estimates and actual amounts.

CBA and County Appraiser Comparison

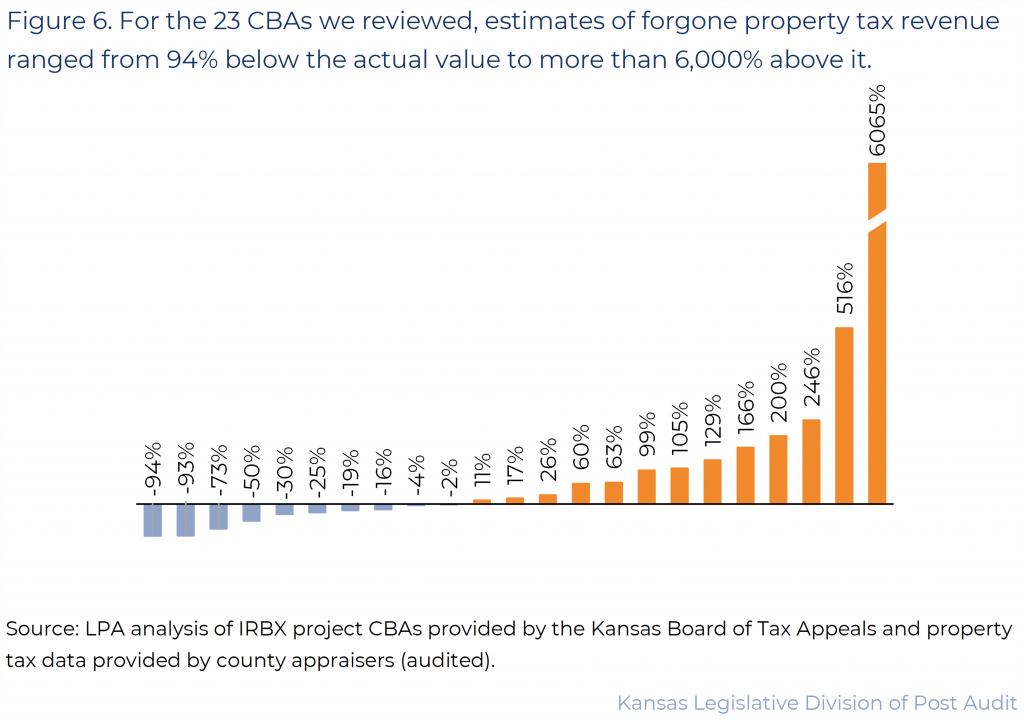

The estimates of forgone property tax revenue in the 23 CBAs we reviewed were between 94% lower and 6,065% higher than official county appraiser values.

- Because CBAs are prepared early in the process and state law does not establish accuracy standards for CBAs, some level of uncertainty is expected.

- Figure 6 below illustrates the wide variation between CBA estimates of forgone property tax revenue and the actual amounts reported by county appraisers. As shown, slightly more than half of the projects overestimated forgone property tax revenue, while slightly fewer than half underestimated it. Overall, the CBAs ranged from underestimating forgone property tax revenue by 94% to overestimating it by more than 6,000%.

- For example, a CBA for constructing a new multi-family residential housing development estimated the project would exempt $5.4 million over 10 years. This estimate was overstated because the project exempted only $2 million. In another case, a CBA for constructing an assisted living facility estimated the project would exempt about $360,000 over 10 years. This estimate was understated because the project exempted $1.3 million over that period.

- We generally didn’t find that factors like bond issuer, bond amount, or CBA preparer resulted in larger differences between estimates of forgone property tax revenue and actual amounts. But our sample was not large enough to draw broad conclusions about the quality of CBAs across all issuers and situations.

Several CBA forgone property tax estimates differed from actual forgone taxes because of incorrect assumptions or changes to the terms of the exemption.

- A few of the CBAs underestimated forgone property tax because they underestimated the property’s final appraised value or the percentage of the property value that would be exempt.

- For example, a CBA for a distribution facility assumed the appraised value of the property would only be about $30 to $40 million in the first year of the exemption period. However, the property appraised for $167 million. This resulted in the CBA significantly underestimating forgone property tax revenue. The exemption is still active, but as of 2025 the CBA’s estimates have been about 90% below actual amounts each year.

- In 2 other cases, the CBAs assumed that a portion of property value would remain taxable and continue generating tax revenue during the exemption period. One CBA for an assisted living facility assumed that 35% of the property value would remain taxable. Similarly, a CBA for a commercial building assumed that 40% of the property value would remain taxable. However, in both cases, 100% of the property value was exempted. As a result, these projects had 2 of the largest underestimations of forgone property tax revenue, with estimates falling 73% and 93% below the actual amounts, respectively.

- Several CBAs overestimated how much property tax would be exempted because they overstated the financial impact of project developments and renovations.

- For example, a CBA for an office building estimated that an investment of $30.5 million on development would result in an appraised property value of $31.2 million in the first year of the tax exemption. But the property only appraised for $19.3 million. This was partly because the project included demolishing an existing building, which did not increase the value of the new building. The exemption is still active, but as of 2025 the CBA estimate was about 60% higher than the actual amount.

- In a similar example, a CBA for an office building renovation project assumed that asbestos removal and a new HVAC system would result in a significant increase in appraised value early in the exemption period. However, these renovations had little effect on the appraised value, which remained relatively flat. The exemption is still active, but the CBA estimate was more than 6,000% higher than the actual amount as of 2025.

- A few CBA estimates were different from actual values because they appear to have been based on IRB values that weren’t finalized at the time the CBA was prepared.

- In one case, a manufacturing facility developer initially requested $145.9 million in IRBs, and the CBA was prepared using that amount. However, by the time the local government issued the bonds, the amount had been reduced to $138 million. This and an assumption that 100% of the investment value would translate into appraised value contributed to the estimate being overstated by 129% as of 2025.

- In a similar example, the local government approved the issuance of up to $20 million for a multi-tenant commercial building. The CBA was prepared using that amount. But when the bonds were issued a few months later, the amount was only $14 million. This and an assumption that exempt taxes would increase by 4% annually contributed to the estimate being overstated by 99% at the time the exemption period ended.

We also identified several CBAs where differences were caused by apparent errors in the CBA or the use of multi-phase CBAs for individual IRBXs.

- We identified apparent errors in several CBAs related to the assessment rates the preparer used. 3 CBAs appeared to use an incorrect assessment rate. All 3 projects were for multi-family residential developments. But the CBAs used the 25% commercial assessment rate instead of the 11.5% residential rate. 2 of the active IRBX projects overestimated forgone property tax revenue by 60% and 105% as of 2025. The third IRBX project is complete and overestimated forgone property tax revenue by 166% at the time the exemption ended.

- 4 CBAs were created for larger multi-phase projects that included investment amounts larger than what was reported on the IRBX applications we reviewed. This led to some of the largest overestimates in the selection we reviewed.

- In one example, $2 million in IRBs were issued for the development of a commercial building. However, this project was part of a larger development that included another property that was not part of the IRBX application we reviewed. The CBA assumed a total investment of $5.9 million for the entire project, not just the $2 million in the IRBX application we reviewed. This was not clearly explained in the CBA and resulted in the estimate of forgone property tax revenue being overstated by about 246% as of 2025.

- In another example, $2.5 million in IRBs were issued for the development of a commercial building. The project was also part of a larger development that included another property with a separate IRBX. The CBA assumed a total investment of $10 million for the entire project, not just the $2.5 million in the application we reviewed. This was not clearly explained in the CBA and resulted in the estimate of forgone property tax revenue being overestimated by about 516% as of 2025.

- Finally, the CBAs we looked at generally assumed a constant mill levy rate and a positive rate of inflation. For example, the CBA for a warehouse project assumed the appraised value and forgone property tax revenue would increase by 1.7% each year. But, in the first few years of the exemption period, the appraised value and forgone taxes decreased by 12%. We didn’t find this to be the primary cause of any differences, but it was a common factor in every CBA we reviewed.

Our results suggest that local governments, CBA preparers, and BOTA do not always closely review the property tax exemption amounts in CBAs.

- BOTA’s review of CBAs is limited to checking whether the required documents were submitted and if the project meets statutory requirements for an IRBX. BOTA does not review the quality of the CBA or determine if the estimates and assumptions are accurate or reasonable.

- Most local government officials we spoke with said they review CBAs in some way. One said they only review summary numbers. Others said they look at the assumptions behind the estimates or speak with CBA preparers to better understand the analysis. Yet, we found that CBAs often used unrealistic assumptions or included clear errors such as incorrect assessment rates, but they were still used to inform IRBX decisions. These findings raise questions about how local governments review CBAs and how much they use them when evaluating projects.

- Most of the local governments we talked to said that inaccurate CBAs don’t significantly impact their decisions to offer a business an IRBX. One official said they mostly disregard the CBA and instead prefer to speak directly with businesses about their plans and expected outcomes. Local government officials see development projects as long-term investments in their communities. Officials said they usually support IRBXs when CBAs show that a project’s benefits outweigh the costs. But they may still approve an IRBX for a project that isn’t expected to produce large returns if the project supports community goals like increasing development, jobs, housing, or retail opportunities. Thus, in some cases CBAs serve more as a required procedural step than as a key tool for judging whether a project is worthwhile.

The problems with CBA estimates of forgone property tax revenue appear to result from several different issues, and some may be difficult or impractical to fully resolve.

- Some issues may be easier to fix like using the correct assessment rate or waiting until project details are finalized before preparing the CBA. Other issues, like estimating how project investment will affect future property value, are more difficult. CBA preparers and county appraisers could work more closely to improve these estimates by identifying which investments are likely to increase property values. However, we don’t know if appraisers would be willing to take on this work. It would require additional time and resources and could raise concerns about the independence of the appraisal process if appraisers are seen as helping create estimates for properties they later have to value.

- Furthermore, factors such as inflation, construction delays, and changing economic conditions can affect project outcomes but are difficult or impossible to predict. As a result, some uncertainty in CBA estimates is unavoidable. Because local officials consider a project’s overall community impact, not just the CBA, when deciding whether to approve an IRBX, local governments and CBA preparers may determine that further refining these estimates is not a practical use of time or resources.

- Finally, we didn’t make a recommendation to address differences between estimated and actual forgone property tax revenue in CBAs because the causes vary from one CBA to the next. CBA preparers use different methodologies, assumptions, and data sources, and our audit did not include a detailed review of those practices. Additionally, our analysis covered only a limited number of preparers, so the findings may not reflect the full range of approaches used statewide.

In 2024, we identified 3 foreign businesses that received $282 million in IRB funds.

There’s no standard federal or state definition of a foreign business, so we developed a definition based on our understanding of legislators’ intent for this audit.

- We were asked to identify how many industrial revenue bonds (IRBs) have been issued for foreign businesses. To do this, we needed to define what a foreign business was. State and federal law don’t provide clear definitions and aren’t consistent. Different federal agencies define foreign differently based on the focus of their work and Kansas law defines any business organized outside the state as foreign.

- In this audit, we defined a foreign business as either being organized outside the U.S. or being a U.S.-organized subsidiary of a foreign business. However, we didn’t examine in detail the relationships between subsidiaries and their foreign parent companies. As a result, we can’t comment on corporate ownership structures, decision-making authority, or the flow of money between subsidiaries and their parent companies as it relates to IRB benefits.

We used several state agency databases to identify foreign businesses that received IRBs in 2024.

- We reviewed IRB data from the Board of Tax Appeals (BOTA) to identify all businesses that received an IRB in calendar year 2024. Local governments are required to file an informational statement with BOTA before IRBs are issued. The informational statements include information about proposed projects including the names of the businesses that will use the bonds. We cross-referenced the business names against data that the Kansas Departments of Commerce and Labor and the Kansas Secretary of State maintain. Due to the time required to request, receive, evaluate, and cross-reference the different data sources, we limited our analysis to 2024.

- All businesses that operate in Kansas must register with the Kansas Secretary of State and provide information on where they were organized (Kansas, another U.S. state, or a foreign country). We requested a list of all active businesses from the Secretary of State and used the list to identify any IRB recipient businesses that were organized outside the U.S. If a company had a foreign jurisdiction of organization, we categorized it as foreign.

- Kansas employers with at least $1,500 in quarterly payroll must file wage reports with the Kansas Department of Labor. These reports include key data for our analysis, such as Federal Employer Identification Numbers (FEINs) and mailing addresses. The Internal Revenue Service (IRS) assigns FEINs starting with “98” to foreign companies, and a foreign mailing address may indicate a foreign connection. We reviewed second-quarter 2024 data to identify businesses with 98-prefix FEINs or foreign addresses. If either of these were true for the businesses in the BOTA data, we categorized them as foreign.

- The Kansas Department of Commerce maintains a confidential internal list of companies that are foreign or have a foreign parent company that they’ve worked with in about the last 10 years. Although the list doesn’t capture all foreign businesses operating in Kansas, it provided a list of confirmed foreign businesses that have operated in the state. If an IRB business appeared on this Commerce list, we categorized it as foreign.

- Finally, we used artificial intelligence to independently review the full 2024 business list from BOTA and identify foreign companies based on our definitions. The results matched our findings, reinforcing our conclusions. But it’s still possible that we may have missed some foreign businesses, especially subsidiaries. Companies with U.S. operations may not report foreign mailing addresses, and U.S.-organized subsidiaries have U.S. jurisdictions of organization and don’t receive foreign FEINs.

In 2024, we identified 3 foreign businesses that received $282 million in IRB funds.

- In 2024, 3 U.S.-organized subsidiaries of foreign businesses received IRBs valued at $282 million. This is a small percentage of the total number of businesses and the total amount of IRBs issued in 2024 (81 total businesses were issued $3.2 billion in IRBs). All 3 projects had IRBXs approved by BOTA in 2025, but they aren’t far enough along for us to determine how much tax revenue will be forgone during the exemption period.

- We didn’t find any instances in 2024 of an IRB going directly to a foreign business. All 3 businesses are U.S.-organized subsidiaries of foreign businesses:

- CAMSO Manufacturing USA, Ltd. is a Delaware-organized company that was a subsidiary of Michelin Group of France, but was acquired by CEAT, an Indian company at the end of 2024. The company received a $60 million IRB to expand its agricultural equipment operations in Junction City.

- Garmin Realty, L.L.C., is a Kansas-organized entity and subsidiary of Garmin Ltd. of Switzerland. The company received a $62 million IRB to renovate 2 buildings on Garmin’s Olathe campus and increase Garmin’s research and development capacity.

- SFC Global Supply Chain, Inc., a Minnesota-organized company and subsidiary of CJ CheilJedang Corporation of South Korea, received a $160 million IRB for a project to build a new Schwan’s refrigerated distribution facility in Salina.

Conclusion

Local governments consistently used industrial revenue bonds (IRBs) to support economic development projects from 2010-2024. During 2010-2024, local governments issued about 955 IRBs worth about $18.3 billion, primarily in larger counties. The number and amount of IRBs issued annually has increased over time, especially in 2024. We estimate the fiscal impact of IRB property tax exemptions was about $1.1 billion in forgone property tax revenue during this time. Nearly all of that amount was forgone revenue to local governments, especially school districts, since property tax is largely a local tax. However, the complete fiscal impact of the IRB program is not known because the other major tax incentive associated with the program—a sales tax exemption—is not tracked and reported by program. Because sales tax is largely a state tax, this is a potentially significant forgone revenue to the state that we, nor the Kansas Department of Revenue (KDOR), can fully quantify.

This audit also revealed several data accuracy issues. As has been noted in other audits, KDOR’s property value data had several problems at the county level. Thus, we could only report at the state level. Further, the Board of Tax Appeals’ (BOTA’s) data did not reflect more than 100 IRB property tax exemption applications for Sedgwick County because the county appraiser did not submit the applications to BOTA. Finally, the cost-benefit analyses prepared by local governments or their contracted parties, frequently included estimated forgone property tax revenue that deviated from the actual amounts reported by county appraisers. The estimates in our selection were between -94% to +6,065% different than the actual amounts.

It’s difficult to recommend specific solutions in these areas. These problems are complicated because they involve a lot of different entities—counties, businesses, third parties—who each do things their own way. The problems are also part of bigger systems. For example, cost-benefit analyses are one of many steps required to issue IRB property tax exemptions, and KDOR’s statistical reports are one of many reports and data systems they use.

Recommendations

- The Kansas Board of Tax Appeals (BOTA) should work with the legislature during the 2027-2028 legislative session to establish a deadline that defines when an IRBX application needs to be forwarded to them after it is received by the county appraiser.

- BOTA Response: Agency Response: BOTA does not object to working with the 2027-2028 Legislature to establish a deadline defining when an IRBX application needs to be forwarded to BOTA for final decision upon receipt of the application by the County Appraiser. BOTA believes that any such deadline would be more appropriately created by the Legislature rather than being created by administrative regulation. BOTA notes, however, that it has no statutory authority over any county appraiser’s office and no access to any county appraiser’s data system, therefore BOTA has no way to confirm that a county appraiser has received an IRBX application unless so notified by the county or by the IRBX applicant.

- Consequently, while BOTA is more than willing to participate with the Legislature to establish the deadline, BOTA has no mechanism to determine whether a county appraiser has complied with such deadline or to enforce a county appraiser’s compliance with any such deadline.

- BOTA should develop a process to identify and track potential IRBX applications. This could include using IRB informational statements to identify when an IRBX application may be filed and when an application they expected to receive is missing

- BOTA Response: BOTA generally does not object to developing some process to track potential IRBX applications. BOTA believes its recently implemented content management system has features that can assist with the process, although ultimately any tracking system would require additional staff time to review instances the system flags as “missing” IRBX applications and to follow up with the parties to enquire as to the status of the application.

- BOTA notes that, at present, IRB informational statements only require parties to identify whether they intend to seek an IRBX exemption, not when they anticipate seeking that exemption. It is possible that, after an IRB statement is filed, the parties could choose not to seek an exemption, or a project could be cancelled in its entirety. Consequently, under the current statutory and regulatory scheme, BOTA’s failure to receive an IRBX application does not immediately raise a red flag. Further, it is not abnormal for a lengthy delay to occur between receipt of an IRB statement and the filing of an IRBX application, because IRBX applications are not submitted to the county appraiser until completion of the project. Each IRB project has a different timeline, and IRB projects can be delayed in development for several years. Therefore, there is presently no single anticipated date or even a typical timeframe after its receipt of the IRB statement in which BOTA could reasonably expect to receive an IRBX application.

- Without the establishment of some kind of deadline where BOTA reasonably should expect to receive an IRBX, any kind of tracking process would be based on BOTA’s selection of arbitrary dates on which to follow up with the IRB parties. BOTA suggests that it would be necessary to add an inquiry onto the IRB informational statement asking the parties to identify when they anticipate submitting the IRBX application to the county appraiser to establish a meaningful tracking process. Although that date would not be binding upon the parties, if BOTA knew when the IRBX application was to be submitted to the county appraiser, and knew how long the county appraiser had to forward the application to BOTA, BOTA could then set a targeted date in its system to follow up on the status of the IRBX.

- The Kansas Department of Revenue (KDOR) should ensure that its Statistical Report of Property Assessment and Taxation and its abstract system contain accurate data. KDOR should improve its data quality control process to identify questionable data submitted by counties, follow up with counties when issues are found, and correct errors when necessary.

- KDOR Response: The development of the Statistical Report has long been a manual process involving significant data entry in the past. PVD has been working in recent months to automate the process and eliminate possible human error. This automation is approximately 80% complete and is expected to be completed prior to the release of the next publication in early 2027.

- As a result of preliminary conversations during this audit process, PVD implemented additional data checklist reviews to address audit recommendations.

- Report and compare the EDX/IRBX capital outlay values with reported preliminary July values on the “Summary Sign-Off” (Summary of values by property class) report.

- Compare any reported PILOT amounts from previous to current year for unusually large differences.

- Due to known exemption reporting issues by counties, PVD has taken steps to address exemption reporting in the CAMA system by adding language to the Appraisal Maintenance Specifications that set requirements for county appraisers to follow.

- The Legislature should consider amending statute to either require and enforce standards about the accuracy of CBAs or consider eliminating the CBA requirement altogether.

Agency Response

Kansas Board of Tax Appeals

June 30, 2026

Via Email

Matthew Fahrenbruch

Senior Performance Auditor

Kansas Legislative Division of Post Audit

Re: Board of Tax Appeals Response to Reviewing the Reporting Accuracy and Fiscal Effects of Industrial Revenue Bonds LPA July 2026

Dear Mr. Fahrenbruch,

The Kansas Board of Tax Appeals (the Board) appreciates the opportunity to file a written response to KLDPA’s Review of the Reporting Accuracy and Fiscal Effects of Industrial Revenue Bonds. The Board likewise appreciates your staff’s openness and professionalism in performing this audit and your communication throughout the process.

The Board does not generally contest the findings or conclusions contained within the report, but submits that additional information may be helpful for the Legislature’s understanding of the issues identified. As a statutorily-created entity, the Board’s powers and authority with respect to industrial revenue bonds and industrial revenue bond exemptions are limited to the powers and authority specifically granted by the Legislature. Although the Board receives informational statements indicating the intent to seek issuance of industrial revenue bonds, it is not directed or empowered by statute to evaluate the contents of the application, determine whether the project is a sound investment, or to follow up in the future to determine whether any given project fulfilled its cost/benefit analysis. Similarly, the Board is not authorized or directed by statute to have a monitoring process to determine whether it has properly received all expected industrial revenue bond exemption applications, nor is the Board directed or empowered to monitor or oversee industrial revenue bond exemptions once it has issued a final decision on the application.

The KLDPA’s review of the industrial revenue bond process has identified certain changes that would help ensure all statutory requirements are met throughout the process. Two of the review’s recommendations address the Board specifically. As explained further in its specific response to Recommendation #1, the Board is happy to work with the Legislature to develop a deadline for a county appraiser to submit an IRBX application to the Board once the county appraiser has received it from the applicant. The Board, however, has no statutory authority over any county appraiser’s office and no access to any county appraiser’s data system. Consequently, the Board currently has no mechanism that it could use to monitor or enforce a county appraiser’s compliance with any such deadline.

With respect to Recommendation #2, the Board is likewise willing to implement a monitoring system to assist with identifying instances where an IRBX application may have been expected, but not submitted. As the Board explains in more detail in its response to that recommendation, however, it is difficult based on the information the Board receives with an IRB informational statement to ascertain precisely when an IRBX application should be expected. IRBX applications are submitted when a project is complete, and projects can take years, have different timelines, are subject to delay, or may be cancelled in their entirety. It does not immediately raise a red flag for the Board, then, if a significant period of time elapses between the Board’s receipt of an IRB statement and the filing of an IRBX application. Local governing bodies are in the best position to determine a project’s potential impacts upon the local community, monitor the project’s progress, and determine whether the project is meeting its stated goals and objectives; therefore, the Board relies upon local governing officials to ensure they are following statutory directives when it comes to IRBs and IRBXs. While the Board believes it can code its system to flag IRB matters with no corresponding IRBX on a certain date, any such “flag” will result in additional administrative work to follow up with the parties to determine the status of the IRBX application. Further, unless parties are required to identify a specific timeframe in which the IRBX application should be expected, the Board’s monitoring system would necessarily be based upon an arbitrary selection of dates on which to follow up.

Again, the Board is happy to work with the Legislature on both recommendations, but believes that additional changes may need to be made to the IRB/IRBX process for those recommendations to effectively address the specific issues raised in the report. The Board thanks KLDPA for its efforts in this matter and looks forward to future conversations with KLDPA and the Legislative Post Audit Committee.

Respectfully submitted,

Kristen D. Wheeler

Chair, Kansas Board of Tax Appeals

Kansas Department of Revenue

June 30, 2026

Chris Clarke

Post Auditor

Kansas Legislative Division of Post Audit

800 SW Jackson St., Suite 1200

Topeka, Kansas 66612

RE: Reviewing the Reporting Accuracy and Fiscal Effects of Industrial Revenue Bonds

Dear Post Auditor Clarke:

Thank you for the opportunity to comment on the audit findings in the Reviewing the Reporting Accuracy and Fiscal Effects of Industrial Revenue Bonds audit report. The Kansas Department of Revenue (Department) commends the Legislative Post Audit (LPA) staff for their work in conducting this important audit.

I wanted to take the opportunity to follow up on Recommendation Number 3 of the audit report concerning the Department. The recommendation states “The Kansas Department of Revenue (KDOR) should ensure that its Statistical Report of Property Assessment and Taxation and its abstract system contain accurate data. KDOR should improve its data quality control process to identify questionable data submitted by counties, follow up with counties when issues are found, and correct errors when necessary.”

KDOR recognizes that the data in the Statistical Report of Property Assessment and Taxation (Statistical Report) is relied upon by many entities and is committed to ensuring its accuracy. Information used to develop the 375 (+) page Statistical Report is submitted to the Department by counties, and the Department relies on the counties’ data submission to create the report. The development of the Statistical Report has long been a manual process involving significant data entry and merging of data. The Division of Property Valuation (PVD) has been working in recent months to automate the process and eliminate possible human error. This automation is approximately 80% complete and is expected to be completed prior to the release of the next publication, which will occur in early 2027.

During the preliminary discussions with LPA regarding questionable data identified during the audit, PVD explained quality control measures already implemented to address data accuracy but, these were not referenced in the final audit report. A previous audit finding indicated not all Industrial Revenue Bond (IRB)/Economic Development (EDX) exemptions were reported in the Statistical Report. Specifically, IRB/EDX exemptions executed after 2017 that excluded capital outlay dollars for school districts were reported correctly, but omitted from the Statistical Report. One particular quality control measure incorporated the exemption data into the latest 2025 update of the report published in early 2026. Both the 2024 and 2025 tax years were included.

To further strengthen PVD’s process and provide additional documentation of these controls, it has implemented additional data checklist reviews which will be shared with counties during PVD’s educational offerings in fall of this year.

PVD will continue to evaluate and enhance its quality control procedures as needed. The following additions have been incorporated into the quality control checklist:

- Report and compare the IRB/EDX capital outlay values with reported preliminary July values on the “Summary Sign-Off” (summary of values by property class) report.

- Compare any reported PILOT amounts from previous to current year for unusually large differences.

Due to known exemption reporting issues by counties, PVD has taken steps to address exemption reporting in the Computer Assisted Mass Appraisal (CAMA) system by strengthening the language in the Appraisal Maintenance Specifications and also adding additional language to the Procedural Compliance Guide. The specifications require all parcels statutorily authorized for exemption, including partially tax-exempt properties receiving a reduced property tax, a rebate or property tax credit, to have an “Exemption Record” created in the CAMA system exemption tracking module. Each record will also have a corresponding “Exemption Type Code” identified on the exemption record. Notable economic incentive programs such as Neighborhood Revitalization Program (NRP), Economic Development, IRB, Reinvestment Housing Incentive District (RHID) and Tax Increment Financing (TIF) programs were specifically cited in the document.

In summary, KDOR has made significant progress in addressing data challenges and strengthening its data quality control processes. While opportunities for further improvements remain, KDOR has demonstrated a strong commitment to identifying issues, implementing corrective measures, and enhancing the overall reliability and integrity of the data received from counties. The collaborative efforts of the team have been instrumental in achieving these advancements, and the work has made a meaningful difference.

Sincerely,

Mark A. Burghart, Secretary

Kansas Department of Revenue

Appendix A – Cited References

This appendix lists the major publications we relied on for this report.

- Industrial Revenue Bond Property Tax Exemptions (March, 2022). Kansas Legislative Division of Post Audit.

- Reviewing Tax-Exempt Real Property and Property Donated to Universities (January, 2026). Kansas Legislative Division of Post Audit.